Chapter 7 and 13 Bankruptcy

Protecting Your Rights for 35 Years

Free Initial Consultation

Why Choose a Chapter 7 & 13 Bankruptcy Lawyer?

⭐ Experience that Counts:

Seasoned Chapter 7 and Chapter 13 attorney Marc P. Feldman has successfully navigated countless cases, helping individuals and families regain their financial stability.

⭐ Compassionate Guidance:

I understand the stress you're under. I provide legal expertise while also the empathy and support you need during this challenging time.

⭐ Tailored Solutions:

There's no one-size-fits-all solution in bankruptcy. I work closely with you to create a personalized Chapter 13 plan that suits your unique circumstances and goals.

⭐ Streamlined Process:

Bankruptcy can be overwhelming, but it doesn't have to be. I streamline the process, handling the paperwork and legalities so you can focus on rebuilding.

⭐ Protection from Creditors:

Once you file for Chapter 13, an automatic stay goes into effect, halting creditor actions and giving you the breathing room you need to regroup.

🌟 Your Path to Financial Renewal Begins Here!

Don't let debt dictate your life. Take the first step towards a brighter financial future by scheduling your FREE consultation today. During this call, expert bankruptcy attorney Marc P. Feldman will:

1. Listen to your situation with understanding and respect.

2. Evaluate your eligibility and explore alternatives to Chapter 13 if applicable.

3. Outline the Chapter 13 process and what you can expect.

4. Answer any questions or concerns you may have.

💼 Take Action Today! Your Debt-Free Tomorrow Starts Now.

Ready to break free from the chains of debt? Chapter 13 bankruptcy lawyer Marc P. Feldman is dedicated to helping you regain control and build a more stable future. Your fresh start is just a click away.

📞 Call now to schedule your free consultation. Don't wait; relief awaits!

Chapter 13 Bankruptcy

Secure Your Fresh Financial Start with Chapter 13 Bankruptcy!

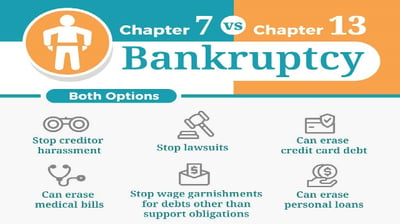

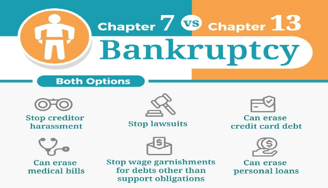

Chapter 13 bankruptcy, also known as a "wage earner's plan," allows individuals with regular income to develop a plan to repay all or a portion of their debts over a period of three to five years. There are various reasons why someone might choose to file for Chapter 13 bankruptcy:

Foreclosure Prevention:

One of the primary reasons for filing Chapter 13 bankruptcy is to prevent foreclosure on a home. The automatic stay that goes into effect upon filing halts foreclosure proceedings and allows the debtor to catch up on missed mortgage payments over the course of the repayment plan.

Debt Repayment:

Chapter 13 allows individuals to create a structured repayment plan to pay off their debts. This is particularly useful if they have a regular income but are struggling with overwhelming debt, as it provides a manageable way to repay creditors over time.

Income Too High for Chapter 7:

Chapter 7 bankruptcy involves liquidating non-exempt assets to repay creditors. If someone has a higher income that exceeds the Chapter 7 eligibility threshold, they might opt for Chapter 13 to avoid liquidation and instead repay a portion of their debts through the repayment plan.

Secured Debts:

Chapter 13 can help with managing secured debts, such as car loans, by allowing the debtor to catch up on missed payments and potentially reduce the interest rate or balance owed.

Don't wait any longer to break free from the burden of debt. Take the first step towards a debt-free life by scheduling a consultation with our Chapter 7 bankruptcy lawyer Marc P. Feldman today. Your fresh financial start is just a call away!

Chapter 7 Bankruptcy

Secure Your Fresh Financial Start with Chapter 7 Bankruptcy!

Filing for Chapter 7 bankruptcy is a significant decision and should be made after careful consideration of your financial situation and consultation with a qualified bankruptcy attorney. Chapter 7 bankruptcy is designed to provide individuals a fresh start by discharging most of their unsecured debts. Here are some common reasons why individuals might consider filing for Chapter 7 bankruptcy:

Overwhelming Debt:

If you have accumulated significant unsecured debts such as credit card bills, medical bills, personal loans, and other debts that you cannot realistically repay, Chapter 7 bankruptcy may provide relief by discharging these debts.

Income Loss:

If you have experienced a substantial reduction in income, such as job loss, pay cuts, or reduced working hours, you may find it difficult to meet your financial obligations. Chapter 7 bankruptcy could help you eliminate or reduce the burden of unmanageable debt.

Foreclosure or Repossession:

If you are facing the threat of losing your home to foreclosure or your vehicle to repossession, Chapter 7 bankruptcy can provide temporary relief by putting an automatic stay on these actions. However, it's important to note that Chapter 7 may not necessarily prevent foreclosure or repossession in the long term if you're unable to catch up on missed payments.

Medical Bills & Expenses:

Medical bills can quickly accumulate, especially in the case of unexpected illnesses or injuries. If your medical debts have become insurmountable, Chapter 7 bankruptcy may offer a way to discharge these obligations.

Don't wait any longer to break free from the burden of debt. Take the first step towards a debt-free life by scheduling a consultation with our Chapter 7 bankruptcy lawyer Marc P. Feldman today. Your fresh financial start is just a call away!

Loan modifications

Loan modification through Chapter 13 bankruptcy is a legal process that allows individuals with a regular source of income to restructure their debts and create a repayment plan under the supervision of the bankruptcy court. Chapter 13 bankruptcy is often referred to as a "wage earner's plan" because it's designed for individuals who have a steady income and want to repay their debts over time rather than liquidating their assets in a Chapter 7 bankruptcy.

Here's how the process generally works:

Filing for Chapter 13 Bankruptcy:

To initiate the process, you need to file a petition for Chapter 13 bankruptcy with the bankruptcy court. This filing will include a proposed repayment plan that outlines how you intend to repay your debts over a period of three to five years.

Loan Modification Request:

As part of your proposed repayment plan, you may seek to modify certain types of loans, such as mortgage loans. Loan modification aims to make the monthly payments more affordable by adjusting the interest rate, extending the loan term, or even reducing the principal balance in some cases.

Approval and Confirmation:

The bankruptcy court will review your proposed repayment plan, including the loan modification request. If the court finds the plan feasible and meets the necessary requirements, it may confirm the plan. This confirmation legally binds both you and your creditors to the terms of the plan.

Implementing the Plan:

Once the plan is confirmed, you will begin making monthly payments to the bankruptcy trustee. The trustee will distribute these payments to your creditors according to the terms of the plan. If your loan modification request was approved, the modified terms of the loan will be reflected in the payments.

Completing the Plan:

You must make all required payments according to the plan over the designated period, typically three to five years. At the end of the plan, if you have made all payments as required, any remaining eligible debts that were not fully paid off may be discharged (eliminated)

Secure Your Fresh Financial Start with Chapter 13 Bankruptcy!

Wage Garnishment & Judgments

Wage garnishment: If you are being sued by creditors, facing wage garnishment, or dealing with other legal actions, filing for Chapter 7 bankruptcy can halt these proceedings and potentially discharge the associated debts.

Legal Judgments: If you've been hit with a significant legal judgment or multiple judgments that you cannot afford to pay, Chapter 7 can discharge many types of judgments, helping you avoid wage garnishment or bank account seizures.

Don't let debt control your life any longer. Take the first step towards a brighter financial future today. Contact Chapter 7 and Chapter 13 bankruptcy lawyer Marc P. Feldman at 973-267-7555 for a confidential consultation. Your journey to financial freedom starts now.

Taxes

There is a common misconception that income taxes are never dischargeable in bankruptcy. In fact, you can discharge some back federal, state, and local income taxes in Chapter 7, Chapter 13, and Chapter 11 bankruptcy. Moreover, the penalties and interest attached to these taxes are dischargeable as well. Determining which back taxes are dischargeable can be a complex process. Nonetheless, it is possible to discharge significant income tax debt in bankruptcy, if your tax debt fits within certain rules.

Take the first step towards a debt-free life by scheduling a consultation with bankruptcy lawyer Marc P. Feldman today.

Foreclosure

If you’re facing foreclosure or are already involved in proceedings, chances are you want to stop this process before your lender takes your home.

You may have heard of other ways to stop foreclosure, but did you know that filing for bankruptcy can provide you with temporary relief? It can! Depending on the type of bankruptcy you use, you can also develop a plan to pay back your mortgage arrears over time, allowing you to get current on your mortgage after experiencing financial hardship.

Whether you file for Chapter 7 or Chapter 13 bankruptcy, creditors must stop all activities intended to seek repayment for debts for as long as the bankruptcy case remains open, including mortgages.

If you file for bankruptcy after receiving a notice that your lender intends to foreclose, the automatic stay prevents your lender from proceeding with foreclosure.

If you are currently involved in foreclosure proceedings, the automatic stay means these must cease for as long as it takes your bankruptcy case to conclude, or until the automatic stay is lifted.,

The automatic stay isn’t permanent. It only persists for as long as your bankruptcy case lasts. This means that if you still owe your mortgage lender arrears after Chapter 7, it can move forward with foreclosure. In some cases, the automatic stay can be terminated prior to the completion of your bankruptcy. For the purposes of this article, we will not examine those situations.

In Chapter 13, you can reorganize your debt into more manageable payments plans. These plans last three to five years, and as long as a bankruptcy filer adheres to its terms, they can either pay off their debt or receive a discharge of remaining debt at the end of the plan.

Chapter 13 is useful for reorganizing mortgage arrears and paying them off over time, which can help you keep your home for much longer than the automatic stay permits. When you follow your Chapter 13 plan, that can mean keeping your home indefinitely.

Your brighter financial future starts here. Call 973-267-7555 to schedule a free initial consultation with bankruptcy lawyer Marc P. Feldman now to take the first step towards freedom from debt and a more secure tomorrow.

Personalized Solutions: I understand that every individual's financial circumstances are different. I will work closely with you to develop a tailored Chapter 13 plan that addresses your specific debts and financial goals. Fill out the contact form to schedule your consultation with bankruptcy lawyer Marc P. Feldman or call now.

Credit card and medical debt

Bankruptcy can offer relief from credit card debt and medical debt by providing individuals with a legal process to address their financial difficulties and potentially discharge or restructure these debts. Here's how bankruptcy can help with credit card debt and medical debt:

Discharge of Unsecured Debt:

In a bankruptcy case, unsecured debts like credit card debt and medical debt may be eligible for discharge. A discharge means that the debtor is no longer legally obligated to repay these debts. Chapter 7 bankruptcy is the most common form of bankruptcy that allows for the discharge of unsecured debts. Once the discharge is granted, the debtor gets a fresh start, and creditors are prohibited from attempting to collect on those discharged debts.

Debt Repayment Plans:

Chapter 13 bankruptcy, also known as a repayment plan bankruptcy, allows individuals to create a structured repayment plan for their debts, including credit card and medical debts. The debtor works with the court to establish an affordable repayment schedule over a period of three to five years. At the end of the plan, any remaining eligible unsecured debts (like credit card and medical debts) may be discharged.

Automatic Stay:

Once a bankruptcy case is filed, an automatic stay goes into effect. This halts all collection activities, including harassing calls from creditors, wage garnishments, and legal actions like lawsuits. This provides immediate relief and allows the debtor some breathing room to address their financial situation.

Negotiation and Reduction:

In some cases, creditors may be willing to negotiate with debtors who are considering bankruptcy. They might agree to reduce the total amount owed or create a more manageable repayment plan outside of bankruptcy.

Protection of Assets:

Bankruptcy laws provide exemptions that protect certain assets from being seized to satisfy debts. This ensures that debtors can maintain a basic standard of living and a fresh start after bankruptcy. While exemptions vary by jurisdiction, they often include essential items like a certain amount of equity in a home, a vehicle, and personal items.